News

What Does Making Tax Digital Mean for Landlords?

The Short Version

If you're a landlord with property income over £50,000 (combined with any self-employment income), Making Tax Digital for Income Tax starts for you in April 2026. Instead of one annual tax return, you'll send HMRC four quarterly updates through compatible software, plus a final declaration at year end.

HMRC estimates 118,000 landlords are in the first wave. If that's you, here's what you actually need to know.

What's Changing?

Currently, you file one Self Assessment tax return per year. Rental income in, allowable expenses out, tax owed calculated, done.

Under Making Tax Digital for Income Tax (MTD for ITSA), that becomes:

- Four quarterly updates of your rental income and expenses, sent to HMRC through compatible software

- One final declaration (similar to your current Self Assessment) due by 31 January

- All records kept digitally - in software, not notebooks or spreadsheets

Quarterly deadlines: 7 August, 7 November, 7 February, and 7 May.

Does This Affect Me?

The threshold is based on your gross qualifying income - that's your total rental income plus any self-employment income, before expenses:

| When | Who's Affected |

|---|---|

| April 2026 | Qualifying income over £50,000 |

| April 2027 | Qualifying income over £30,000 |

| April 2028 | Qualifying income over £20,000 |

Key details:

- Employment income (PAYE) and pensions don't count. It's only self-employment and property income.

- Joint ownership: If you own a property 50:50 with a spouse, your qualifying income is your 50% share of the gross rent.

- Multiple properties: All your rental income is combined. Three properties each bringing in £18,000 puts you at £54,000 - you're in the first wave.

Why Landlords Are Frustrated (And Rightly So)

This is hitting landlords at a particularly bad time. Between the Renters' Rights Bill, mortgage rate changes, and Section 24 tax relief restrictions, the last thing most landlords need is more admin. Here's what's actually annoying people:

"I get rent paid into my account monthly. Why do I need software for that?"

Your income side might be simple - 12 monthly rent payments. But MTD requires you to track expenses digitally too. Maintenance costs, letting agent fees, insurance, mortgage interest (the allowable portion), repairs, ground rent, service charges. All of it, categorised and dated, in compatible software.

"I only have one buy-to-let. This feels like overkill."

If your one property generates over £50,000 gross rent (or you have self-employment income that pushes you over), you're caught. Even if your actual profit after mortgage interest and expenses is modest. The threshold is gross income, not profit.

"I've been managing my property books in a spreadsheet for 15 years."

Spreadsheets can technically still work, but only with bridging software that creates a "digital link" to HMRC. You can't manually copy numbers from Excel into HMRC's system. For most landlords, switching to proper software is less hassle than rigging up bridging solutions.

"My expenses are lumpy - one big repair bill, then nothing for months."

Quarterly reporting means you'll sometimes submit a quarter where you've spent more than you've earned (big repair, new boiler, roof work). That's fine. MTD is a running record, not a final bill. The year-end declaration is where everything balances out.

What You Need to Track Each Quarter

Income:

- Rent received (date, amount, which property)

- Any other property income (parking, storage, service charges passed on)

Expenses (these reduce your tax bill):

-

Letting agent fees - typically 8-15% of rent

-

Maintenance and repairs - plumber call-outs, broken appliances, redecorating between tenants

-

Insurance - landlord insurance, buildings insurance, rent guarantee insurance

-

Mortgage interest - the tax credit portion (20% of finance costs since Section 24)

-

Ground rent and service charges - if applicable

-

Accountant fees - yes, the cost of compliance is itself tax-deductible

-

Travel to the property - mileage for inspections, viewings, meeting tradespeople. 45p per mile for the first 10,000 miles

-

Legal and professional fees - lease renewals, eviction costs, safety certificates

-

Safety compliance - gas safety certificates, EPC, electrical checks, smoke/CO alarm testing

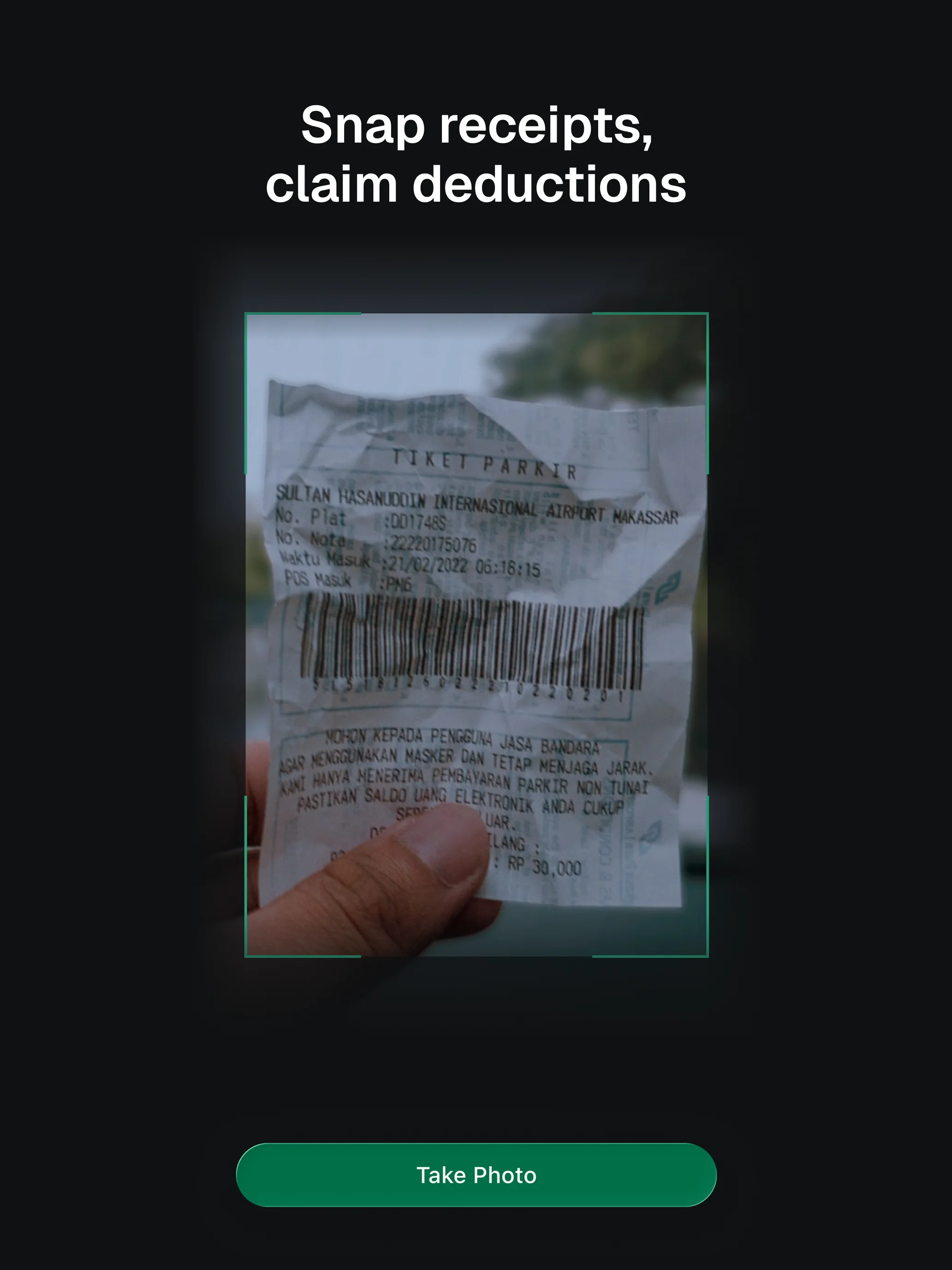

Most landlords we talk to are surprised by how much they're entitled to claim. When you're tracking everything in real time rather than trying to reconstruct 12 months of expenses in January, you capture a lot more.

If You're Also Self-Employed...

Here's where it gets properly annoying. If you have BOTH rental income AND self-employment income, you need to submit separate quarterly updates for each income source.

That means 8 quarterly submissions per year, plus the final declaration. If you're also VAT-registered, add your VAT returns on top.

Some landlords who are also sole traders could be filing 10+ submissions a year to HMRC. It's a lot. Having software that handles both in one place is pretty much essential.

Picking the Right Software

What to look for as a landlord:

Property-specific features - Can it handle multiple properties? Track income and expenses per property? Handle joint ownership splits?

MTD compatible - Must be on HMRC's compatible software list and able to submit quarterly updates directly.

Simple enough to actually use - If the software requires accounting knowledge, you'll end up paying your accountant to operate it anyway.

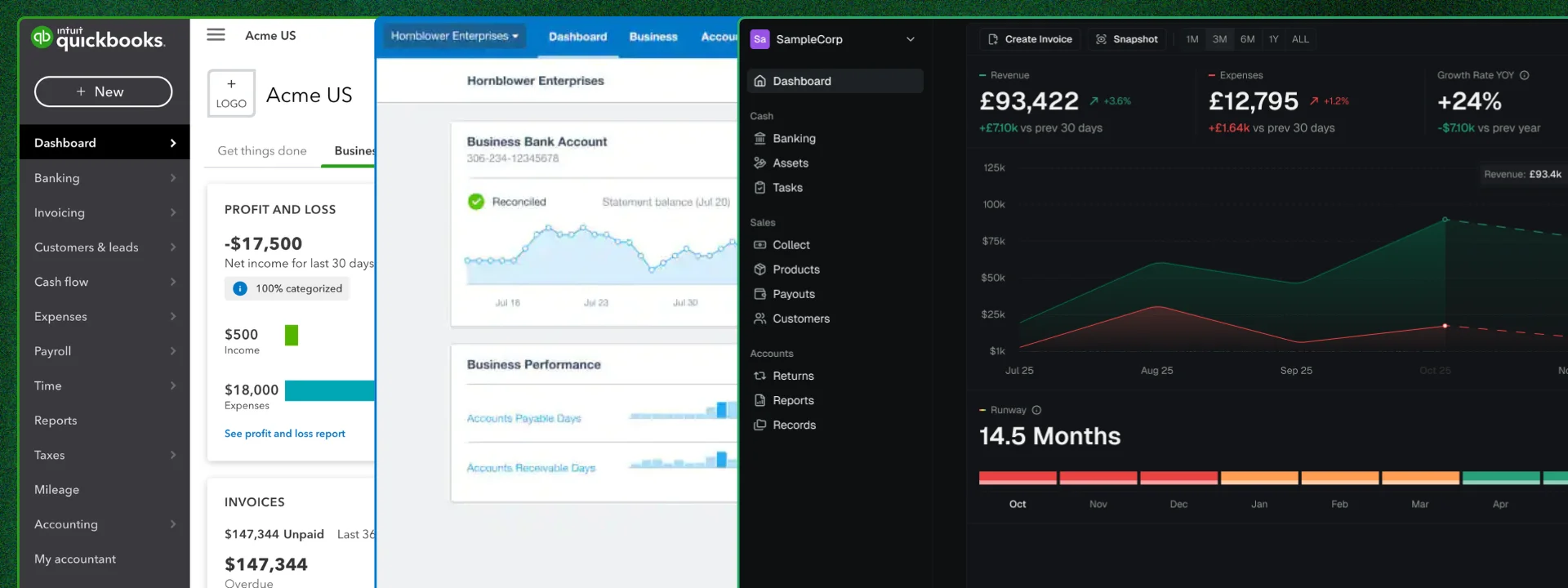

Xero - Powerful and widely used, but it's general accounting software. You'll need to set up tracking categories for each property. From £16/month. Works well if your accountant already uses it.

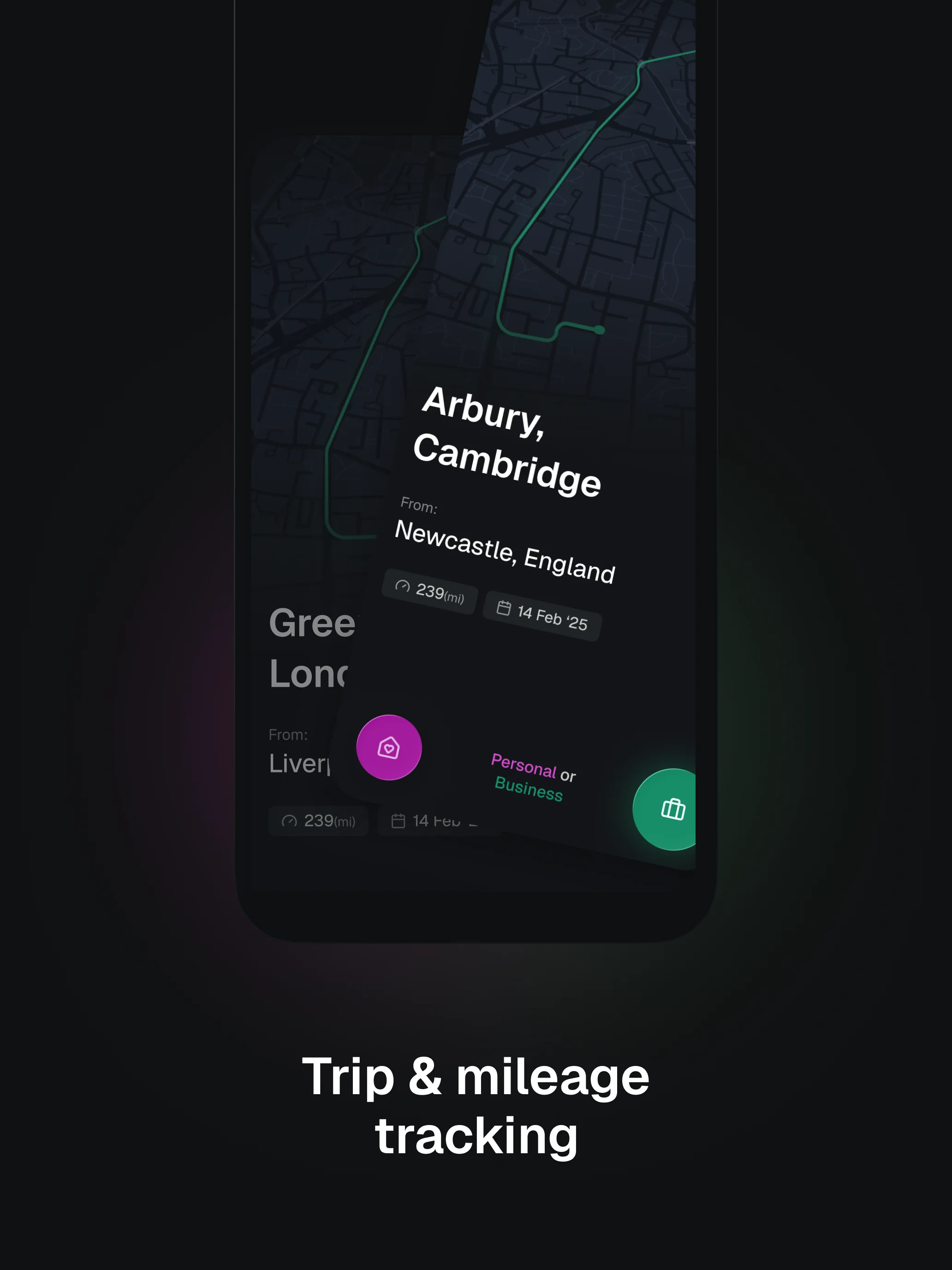

Hammock - Built specifically for landlords. Handles per-property tracking and MTD submissions. Worth a look if property is your only income.

Aarvo - If you're a landlord who also has self-employment income, Aarvo handles both in one place. Receipt scanning, mileage tracking, expense categorisation that doesn't require an accounting degree. It's designed to make the quarterly updates feel like a 5-minute check rather than an afternoon of work.

The Penalty System

HMRC's new points-based penalties:

- 1 point per missed quarterly submission

- 4 points = £200 fine

- Late payment: Interest from day 1. 2% penalty after 15 days late, another 2% after 30 days.

Grace period: HMRC has confirmed no penalty points for late quarterly updates in the 2026/27 tax year. But the final declaration penalties still apply, and the grace period won't last.

FAQ

My rental income is under £50,000 - should I still prepare?

Yes. The threshold drops to £30,000 in 2027 and £20,000 in 2028. Getting set up now means you're building good habits before it becomes mandatory.

I use a letting agent who handles everything - does this change?

Your letting agent manages the property, not your tax reporting. You (or your accountant) still need to keep digital records and submit quarterly updates to HMRC. Your agent's monthly statements are useful source documents, but they're not a substitute for MTD-compatible software.

What about furnished holiday lets?

Furnished holiday lets have specific tax rules, but they're still rental property income. If your total qualifying income exceeds the threshold, MTD applies. The quarterly reporting requirements are the same.

I own properties jointly with my spouse - how does the threshold work?

Each person reports their share. If you own a property 50:50 generating £80,000 gross rent, each of you has £40,000 qualifying income. Neither of you is in the April 2026 group individually (unless you have other qualifying income that pushes you over £50,000).

Can my accountant do all of this for me?

Yes, but expect the relationship to change. Instead of one annual catch-up, you'll need quarterly coordination. Many accountants are setting up ongoing digital access to clients' records so they can review and submit on your behalf. This will likely cost more than your current annual fee.

Get Ahead of It

MTD is one more thing on the pile for landlords. But the landlords who get their digital records sorted early tend to end up claiming more expenses, having fewer tax surprises, and spending less time on admin overall.

If you want a simple way to track your property income and expenses without feeling like you need an accounting qualification, take a look at Aarvo. Most landlords find they claim back more in missed expenses than the subscription costs - it pays for itself.

Related reading: Also self-employed? See our guide on what MTD means for sole traders. Work in construction? Check what MTD means for CIS subcontractors. Explore Aarvo's documentation or see our pricing.

This guide references official HMRC guidance on MTD for ITSA and is accurate as of March 2026. Tax rules change - always check GOV.UK for the latest.

Aarvo Team

Product updates and insights

Related articles

View all news →

What Does Making Tax Digital Mean for CIS Subcontractors?

Making Tax Digital for CIS subcontractors from April 2026. Your CIS deductions don't change, but quarterly reporting to HMRC is new. Here's what to do.

Aarvo · 26 Mar 2026

What Does Making Tax Digital Mean for Sole Traders?

Making Tax Digital for sole traders starts April 2026 if you earn over £50,000. What's changing, what you need to do, and how to pick the right software.

Aarvo · 23 Mar 2026

The Edge You Never Knew You Needed

10 years of building businesses without understanding my own numbers. That frustration became Aarvo. Here's the story from our founder.

Aarvo · 12 Nov 2025